More Than a Paycheck,

REFUSING to PAY for WAR

August/September 2015

Contents

- The Hobby Lobby Decision and War Tax Resisters by Peter Goldberger

- The Mice Will Play by Bill Ramsey

- Counseling Notes Preemptive Letters • Miscellaneous Issues

- Many Thanks to everyone who supports NWTRCC with their volunteer time or financial donations and to the following groups for recent donations

- Network List Updates

- War Tax Resistance Ideas and Actions Out and About • Peace Patriot • Making It Public • Closing the Chapter, Not the Book • 30th Anniversary for New Englanders!

- Resources Recent Talks Now Online • Bumperstickers

- NWTRCC News Thanks, Larry! • Inspiration for A Better World • Meet WTRs Somewhere in the U.S.

- PROFILE War Tax Resistance and Other Paths to a Better World By Sylvia Metzler

Click here to download a PDF of the August/September issue

The Hobby Lobby Decision and War Tax Resisters

by Peter Goldberger

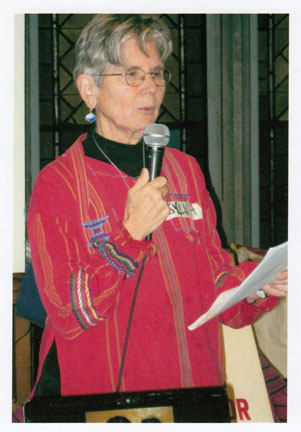

Editor’s note: This is an edited selection from a talk by attorney Peter Goldberger, given at the NWTRCC gathering at the Earlham School of Religion, November 8, 2014. Presented here is about one-quarter of Peter’s talk, meant to entice you to listen to or read the full presentation online or ask for a copy from NWTRCC. Peter’s talk begins with background for his arguments regarding the Hobby Lobby decision. He discusses his interpretation of legal issues related to civil disobedience and conscientious objection, then moves into the “free exercise” section below and into Obamacare, with more detail on the decision and what it means for WTRs than we can present here. Links to the text or video are on the home page at nwtrcc.org.

Peter Goldberger speaking at Earlham School of Religion. November 2014. Photo by Ruth Benn. The Free Exercise Clause is the part of the First Amendment that assures each adherent of a minority faith the right to practice his or her religion without state interference. Taken literally, the Free Exercise Clause would seem to establish a general right of conscientious objection to any and all laws for religious people. When a law requires everyone to engage in certain conduct, and that conduct violates some people’s religion, or the law prohibits conduct that is required by some people’s religion, doesn’t the law violate the Free Exercise Clause as applied to those people? Well, logic would say yes, but for all of its history the Supreme Court has said no to that question.

Peter Goldberger speaking at Earlham School of Religion. November 2014. Photo by Ruth Benn. The Free Exercise Clause is the part of the First Amendment that assures each adherent of a minority faith the right to practice his or her religion without state interference. Taken literally, the Free Exercise Clause would seem to establish a general right of conscientious objection to any and all laws for religious people. When a law requires everyone to engage in certain conduct, and that conduct violates some people’s religion, or the law prohibits conduct that is required by some people’s religion, doesn’t the law violate the Free Exercise Clause as applied to those people? Well, logic would say yes, but for all of its history the Supreme Court has said no to that question.

The Supreme Court has never wavered from the position that the Free Exercise Clause “embraces two concepts: freedom to believe, and freedom to act; the first is absolute, the second, in the nature of things, cannot be.” And guess what case they said that in? The 1878 Reynolds decision, ruling against a Mormon for engaging in polygamy. That’s the foundation of American religious freedom law under the Free Exercise Clause.

The Mormon cases have not been undermined since the 1870s. In Gillette v. United States, 1971, a hundred years later, the Supreme Court said there is no constitutional right under the Free Exercise Clause to be a conscientious objector [C.O.], either under the draft or the military — none. The rights of conscientious objectors are those granted by statutory or administrative law, and nothing more. …[T]here was no conscientious objector provision for people who changed their beliefs after joining the military until 1965, and hardly a C.O. provision under the draft before 1940—and not a very good one until 1948, which still had plenty of problems.

In particular, the Supreme Court in the Gillette case said that the government could choose to limit C.O. status to those who oppose all wars, like the Quakers and Mennonites who had lobbied for the law to be passed — a law that was written to basically describe their own belief system — and not Catholics or others who subscribe to a “just war” theology.

Then in 1982 the Supreme Court upheld the limitations on the way Congress had drafted the exemption that it grants to groups like the Amish, who object on religious grounds to participating in Social Security. It’s a case called Lee. [T]alking about the Amish and Social Security, the Supreme Court repeated a line used by a concurring justice in an opinion 50 years earlier about compulsory ROTC in the University of California system, saying that the Free Exercise Clause “obviously” would not support a pacifist’s claim to be exempt from paying taxes that support war-making or military preparations.

The high water mark for the most generous interpretation of the First Amendment Free Exercise Clause was an opinion in 1972 by the Nixon-appointed Chief Justice, Warren Burger, for a nearly unanimous court, in a case called Wisconsin v. Yoder, in which the court sustained the Free Exercise claim of Amish parents to withdraw their children from school after eighth grade, even though they were below the age of compulsory schooling. And the court’s decision combines discussion of the rights of families, the primary role of parents in child upbringing, so it’s not even premised entirely on religious freedom grounds. A year later, applying that precedent, a federal judge in Philadelphia ruled that the American Friends Service Committee was protected by the Free Exercise Clause from having to withhold income taxes from its war-objecting employees. That decision was overturned by the Supreme Court in 1974 on procedural grounds, leaving the precedent in limbo. For nearly 20 years after the Yoder decision in 1982, the Supreme Court continued to say that this is the test that they’re applying, but they never actually ruled in favor of a religious objector in any other case. They found some reason, in every case they took, to rule against the individual and in favor of the state.

And then in 1990 the Supreme Court did a U-turn. They abandoned the pretext of the Yoder case entirely in a case called Smith v. Oregon, written by Justice Scalia. The Smith decision upheld a denial of unemployment compensation to Native American drug and alcohol counselors who had applied for unemployment compensation benefits after losing their jobs in the state of Oregon. Why were they fired? Because they used peyote in their religious ceremonies. The court declared a new rule. The court said in 1990, in the Smith case, that the Free Exercise Clause does not require any religious exemption from a generally applicable law, so long as that law is not designed to interfere with religion, and it doesn’t discriminate against particular religions.

The religious community saw the Supreme Court decision in Smith as a major threat to freedom of conscience, and an amazing coalition of groups—conservative, progressive, and everything in between, from the religious establishment and the religious fringe—got together and lobbied for the creation of something called the Religious Freedom Restoration Act (RFRA). In 1993 that law was approved, and it went into effect in 1994. This was a law passed by Congress that attempted to re-establish by legislative fiat the same standard that the Supreme Court had been using at the high water mark of its Free Exercise jurisprudence, that is, in Yoder. Congress said, This is the test that courts have to apply to individuals who object to being required to comply with any state or federal law to which they have a religious objection.

The rule established by RFRA was basically that an individual objection to compliance with any law has to be accommodated if it is possible to do so. The way the RFRA rule is framed is in these terms: the religious objection has to be honored unless (a) the law serves a compelling governmental interest, and (b) the infringement on conscience is the least restrictive alternative for dealing with the problem of objection — the least restrictive of individual liberty that is feasible. That’s a very strict test.

Health Care, Corporations, and Taxes for Peace

So, comes now 2012, 2013, and Congress passes — just barely — a major reform of the American health insurance system. The Affordable Care Act (ACA) has a provision making churches exempt from the birth-control coverage aspect of the law, if they object on religious grounds. Further, nonprofit, religiously affiliated organizations are provided an opportunity to say they are conscientious objectors, that they have a religious belief against some or all forms of birth control, and cannot in conscience provide these forms of birth control to their employees. And then, in that instance, there’s a side-stepping mechanism, and the insurance company has to provide those employees—the women, mostly — of those religiously affiliated nonprofits with the coverage directly.

[Hobby Lobby and Conestoga Wood Specialties — for-profit corporations owned by religious families — brought cases to court arguing that they should get the same exemption that is given to religious nonprofits.] In one federal appeals circuit, they lose their case, because corporations don’t have a right to free exercise of religion under RFRA, says the court. Corporations don’t have religious consciences or beliefs. In the Tenth Circuit, in another part of the country, on the other hand, Hobby Lobby wins. So the issue goes to the Supreme Court, because there’s a conflict between the two regional appeals courts. In June 2014, the Supreme Court decides in favor of the corporations.

What does it mean for tax resisters? Some commentary that I read on the internet, for example, right afterward, said, “Oh, this means we don’t have to pay taxes if we have a religious motive for not paying.” Well, let’s start with the fact that that very same quote from that 1982 Amish case is in the Hobby Lobby decision, again:

Our holding in Lee turned primarily on the special problems associated with a national system of taxation. We noted in that case that the obligation to pay a Social Security tax is not fundamentally different from the obligation to pay income tax. Based on that premise we explained that it was untenable to allow individuals to seek exemptions from taxes based on religious objections to particular government expenditures. If, for example, a religious adherent believes war is a sin, and if a certain percentage of the federal budget could be identified by those individuals as being devoted to war-related activities, such individuals would have a similarly valid claim to be exempt. The tax system could not function if denominations were allowed to challenge the tax system because payments were made by the government and spent in a manner that violates their religious beliefs.

Well, you may be thinking, Lee was a Free Exercise case. RFRA grants rights that are stronger than Free Exercise, remember? Justice Alito’s decision continues:

Lee was a Free Exercise case; not a RFRA case. But if the issue in Lee were analyzed under RFRA, the fundamental point would be there is simply no less restrictive alternative to the categorical requirement to pay taxes. Because of the enormous variety of government expenditures funded by tax dollars, allowing tax-payers to withhold a portion of their tax obligations on religious grounds would lead to chaos.

This is the Hobby Lobby case quoting the Lee decision, the Amish Social Security decision, although it is completely not a case that is presented before them, and they usually go out of their way not to decide cases other than those which are, strictly speaking, being presented and requiring decision — this is the only issue that they go out of their way to speak about in the decision, other than the decision that is before them.

Well, does that mean that someone could not come to court and say, “We have this idea called the Religious Freedom Peace Tax Act, in which, for those who would be satisfied by it, their money would be channeled and segregated into non-military uses, and they would pay the full amount of tax.” Doesn’t that answer the objection that’s being made there?

So it seems to me, to start out with something positive, that it is arguable that RFRA, as interpreted by the Supreme Court, makes the Peace Tax Fund Act unnecessary, that the Peace Tax Fund Act has been enacted, and it is called the Religious Freedom Restoration Act, unless the government can show that that system wouldn’t work, because it’s a system that generates all the same amount of tax money. Just a thought.

Second, the Supreme Court points out that RFRA gives a broad definition of “exercise of religion,” broader than had ever been articulated by the Supreme Court in a First Amendment case. Specifically, it defines “exercise of religion” as “any action which is impelled by the person’s religious belief, whether or not compelled by or central to that belief.” This definition of religious entitlement to exemption is inconsistent with the military conscientious objector laws, which in my opinion are invalidated by RFRA for being too narrow, for discriminating against certain beliefs, like “just war” theory, which RFRA does not allow, and for requiring that the belief of a military conscientious objector seeking discharge be central — not just religious, but at the center of that person’s religion. That’s flatly inconsistent with RFRA as articulated in Hobby Lobby. The decision points out, for example, that the business practices of a religious person can be an exercise of that person’s religion — obviously not the center of that person’s religious life, but an expression, perhaps, of the person’s religious life. That exact point, of course, is essential to the holding in Hobby Lobby.

I can’t say that my Peace Tax Fund idea is definitely correct. I can’t say the invalidation of the narrow military C.O. rules is definitely correct. But these are serious arguments. These are not fanciful arguments. They are directly predicated on the reasoning of the Hobby Lobby decision interpreting the RFRA statute which, by its terms applies to all federal agencies.

Note: This text was heavily edited. Please listen to or read the full talk, linked at nwtrcc.org, or ask for a copy from the NWTRCC office.

Peter Goldberger is an attorney in Ardmore, Pennsylvania, and the longtime legal consultant to NWTRCC.

The Mice Will Play

Soy beans have given way

to busy yellow Cats.

Beans plowed under as

Cats go round and round,

pushing and packing good earth,

clearing the way for a new generation,

for the planting of sanctioned terror,

a second round of readiness,

to threaten all generations.

The merry band of folks,

like mice file into a field,

meandering toward the Cats,

sowing wildflowers as they go.

Through deep mud they trod

into the forward path of one Cat.

and securely surround it.

Then one detains another Cat

and the worker Cats fall silent

across the field’s expanse.

While the Cats are waylaid,

the mice will play.

And for a portion of minutes,

the only movement

across this piece of earth is

the silent sprouting of wildflowers.

By Bill Ramsey Kansas City, August 16, 2010

Built on a soybean field and now operational, the Kansas City Plant makes parts for nuclear weapons. The “mice” are still actively protesting the plant and nuclear weapons. For more information see peaceworkskc.org.

Counseling Notes:

Preemptive Letters

A resister in Oregon contacted the NWTRCC office recently because he had received a “frivolous penalty warning letter” from the IRS and wasn’t sure what to do. The letter starts:

This is in reply to your correspondence received April 29, 2015. We have determined that the arguments you raised are frivolous and have no basis in law. Federal courts have consistently ruled against such arguments and imposed significant fines for taking such frivolous positions. If you persist in sending frivolous correspondence, we will not continue to respond to it. Our lack of response to further correspondence does not in any way convey agreement or acceptance of the arguments advanced…

The resister did not enclose a letter when he filed. Instead, he sent his letter of conscientious tax refusal to the IRS Commissioner’s office in D.C., which NWTRCC has recommended as a way to avoid frivolous correspondence from the IRS. Perhaps some history from this resister triggered the warning letter, or did the Commissioner’s office forward his letter to the “frivolous office” in Ogden, Utah? Or is this a new preemptive tactic by the IRS? We’re not sure, but in any case, advice from the Taxpayer Advocate Service is that there is no need for (nor should) the taxpayer respond.

Miscellaneous Issues

At the May Counselors’ Training in Milwaukee, we used the Practical WTR Series as our guide. A few things from the session were mentioned in the last issue, and here are a few more:

- Questions of social security levies always come up. The automatic amount the government can levy for a federal debt is 15%, although we hear regular reports from resisters in this category that the levy seems to come and go with no rhyme or reason. As far as we know, only one person in our network has 50% taken from her check after an agent already active on her case filed a standard salary levy against her Social Security payments. The ongoing 50% levy was allowed despite appeals.

- Some in our network also refuse state taxes. Consensus was that states are more enthusiastic collectors than the federal government. NWTRCC cannot track information for each state, but we will try to refer you to others in your area who might have experience with your state.

- We got tangled up in the issue of setting up an LLC — limited liability corporation — as a way to shift individual income to a business. NWTRCC counselors are not well versed in this area. Some in our network have success with cooperative structures, but because states play a major role in business structures, many recommended seeking advice from an accountant or lawyer.

- Practical #2, “To File or Not to File an Income Tax Return,” includes philosophical arguments. One suggestion was to add “The State has no right to exist” to the “reasons to not file” section.

Many questions can be answered by reading the Practical Series — and your suggestions and updates are continually needed and welcome. The booklets can be read or downloaded on the NWTRCC website “Publications” page or ordered from the office.

Many Thanks

We are very grateful for a bequest from the estate of long-time NWTRCC supporter Iris Alexander, who lived in Buffalo. She died at age 86 in November 2014.

Thanks to everyone who sent donations in memory of Juanita Nelson

Special thanks for the grant from The James R. & Mary Jane Barrett Foundation

Affiliate fees and support from alternative funds are a fundamental part of NWTRCC‘s durability. Thank you to:

War Resisters League National Office

Metro Atlanta Conversion Fund, which is closing their account and donated the balance to NWTRCC

Network List Updates

The Network List of Affiliates, Area Contacts, Counselors, and Alternative Funds is updated and online on our contacts and counselors page, or contact the NWTRCC office, nwtrcc@nwtrcc.org or toll free: (800) 269‒7464, if you would like a printed list by mail.

Please note: We are in the process of upgrading our website. Links in this issue are to our current site and may change early in the fall. You will find everything at nwtrcc.org. Just hunt a bit through the new menus.

Don’t forget, you can find us on

Facebook • Twitter • YouTube • Pinterest

and join our discussion listserve

Click on the icons at nwtrcc.org

Advertising rates for this newsletter can be found on our newsletter advertising rates page or contact the editor at (800) 269‒7464.

War Tax Resistance Ideas and Actions

Out and About

Peg Morton attended the Fellowship of Reconciliation 57th Annual Northwest Regional Conference at Seabeck July 2–5. This year she was excited that there was a special time when people could visit the information tables without missing other events. Peg found “a flowing group of people at my peace tax table the entire time! Plus people approached me throughout the conference.” A frequently asked question was “how many WTRs are there?” We’ll entertain ideas from any of you who can figure out how to take a count of war tax resisters in the U.S. For many years we have said 2,000 to 8,000, extrapolated to some extent from the number of people on our national mailing lists along with people in touch with our affiliate groups around the country.

Peace Patriot

Ed Kale was at the front of the marching band at the Fourth of July parade on Madeline Island, Wisconsin. About 3,000 people turned out to participate in or watch the parade. In response to his shirt and sign, Ed heard lots of good comments, including a woman who said, “All we do is pay for war in this country.” If you find yourself on Madeline Island be sure to look for Ed at his kayak rental business, which features a sign on the counter that says “1% OWNING 90% IS FATAL FOR DEMOCRACY.”

Ed Kale was at the front of the marching band at the Fourth of July parade on Madeline Island, Wisconsin. About 3,000 people turned out to participate in or watch the parade. In response to his shirt and sign, Ed heard lots of good comments, including a woman who said, “All we do is pay for war in this country.” If you find yourself on Madeline Island be sure to look for Ed at his kayak rental business, which features a sign on the counter that says “1% OWNING 90% IS FATAL FOR DEMOCRACY.”

Making It Public

“A Time to Speak up for New Budget Priorities” was the title of a pre-tax day event sponsored by Budget for All! and held at the Old South Church in Boston on April 11. The event supported the Congressional Progressive Caucus’ People’s Budget and provided a community platform on how taxpayers’ money should be spent. Featured speakers were Mel King, Jimmy Tingle, Barbara Madeloni, Jamie Eldridge, Jill Stein, and others representing a range of labor, community, faith, and political leaders, including:

My name is Mary Regan and I have been a war tax resister since 1983, when I decided that I could not in good conscience participate in killing and destruction funded with our tax dollars. I pay about half of my federal taxes because about half of the U.S. discretionary budget goes to pay for past, current or future killing and war.

New England War Tax Resistance, a group of Boston area people who refuse to pay some or all of their federal income taxes in order to oppose the funding for wars, weapons, and killing, is proud to announce the donation of $4,500 to local organizations working for a more just and peaceful society.

This donation, money not paid to the federal government, is redirected to efforts that are seen by our members as a better use of our common fund than the military budget.

Organizations that received the grants were the Prison Birth Project, Massachusetts Alliance Against Predatory Lending, Association of Haitian Women in Boston, City School, Youth Justice & Power Union, and the journal New Politics. A video with selections from the program, including Mary at 19 minutes, is online at budget4allmass.org.

Closing the Chapter, Not the Book

Kudos to Quaker attorney Bob Kovsky of San Francisco, who worked for seven years on a legal suit I brought against the IRS claiming that as a Quaker, I was subject to misdirection, threat and harassment by the IRS, when I honestly and openly followed the precepts of my Christian church in refusing voluntarily to pay for war. The case moved back and forth between district and appellate courts for years. Always rejected out of hand, no court hearing was ever scheduled. Bob and I have finally laid down this effort.

For me, giving up the struggle in the courts involves “closing the chapter but not the book,” as my colleague in war tax resistance, Ruth Paine, put it. Along with others in NWTRCC, I see recent wins for religious freedom in the Supreme Court as possible precedents for war tax resisters to build on. The success of plaintiffs in the Hobby Lobby case, in Holt vs. Hobbs, and in similar cases may indicate that this conservative court respects some kinds of law-challenging decisions when they are based in solid religious faith and practice.

But the road is not yet clear for religious tax resisters. Conscientious resisters to mandatory military enlistment have been offered “alternative service” options since World War II or earlier. Those conscientiously opposed to war taxes need a similar “alternative tax” option. The Peace Tax Fund campaign has tried for years to get Congress to offer such an alternative. Perhaps this is the historical moment for some new ideas and energy in that campaign. I am hoping others will join me in seeking out the opportunities.

— Elizabeth Boardman, Santa Rosa, California, eboardman@sbcglobal.net

30th Anniversary for New Englanders!

The New England Gathering of War Tax Resisters and Supporters celebrates its 30th anniversary October 16-18, in Amherst, Massachusetts.

Everyone is welcome to attend — not just to celebrate but to join in exercises to revitalize collective action toward successfully meeting common objectives. “Social technologies,” such as World Cafe and Open Space, will be used to chart a course that enhances the role of WTR in bringing about the world we want. The weekend begins on Friday with dinner, ends with lunch on Sunday, and will include a talk on community and resistance by Frida Berrigan.

Expect good meals, good company, and strategizing with an eye on success. For more information, please contact Daniel Sicken, PO Box 8011, North Brattleboro, Vermont 05304, (802) 387-2798, dhsicken@yahoo.com.

Resources

Recent Talks Now Online

From the NWTRCC Gathering at the Earlham School of Religion, November 2014, at vimeo.com/album/3451940:

- What does the Supreme Court’s Hobby Lobby decision mean for war tax resisters? by attorney Peter Goldberger

- Quakers and the war tax concern: Unfinished business? by Professor Lonnie Valentine

- Strategizing for social change in 21st century America by Professor Joanna Swanger

From the NWTRCC Gathering in Milwaukee, May 2015, at nwtrcc.org/meetings.php:

- Afghan Peace Volunteers presentation with Patrick Kennelly

- Methods of Resistance panel with Milwaukee activist Mary Watkins, peace activist and man-of-many-hats George Martin, and Ruth Benn, NWTRCC Coordinator

Bumperstickers

If You Want Peace, Stop Paying for War! You don’t need a bumper—see the “peace patriot” photo above! 11″x 2″, blue ink on white

Defund Militerrori$m with small type: “This sticker (and 999 others) paid for with ‘tax obligations’ redirected from war.” White letters on black, 9″ x 2½”

Get both stickers by mailing $1 to NWTRCC, PO Box 150553, Brooklyn, NY 11215.

NWTRCC News

Thanks, Larry!

NWTRCC has a fiscal sponsor, a 501(c)3 organization that accepts tax deductible contributions for our educational work. For many years, Resources for Organizing and Social Change (ROSC) has provided this service, and for all those years up to June 30, 2015, ROSC has been staffed by Larry Dansinger. But now Larry has decided to head into something called “non-retirement,” and Sass Linneken is taking over at ROSC. Larry is a longtime WTR and keeps the Maine WTR Resource Center alive. His recent bumpersticker idea: “Divest from the Pentagon” with subtitle “don’t pay federal income taxes.” We are grateful for Larry’s support and assistance to NWTRCC for so many years and look forward to working together in new ways.

NWTRCC has a fiscal sponsor, a 501(c)3 organization that accepts tax deductible contributions for our educational work. For many years, Resources for Organizing and Social Change (ROSC) has provided this service, and for all those years up to June 30, 2015, ROSC has been staffed by Larry Dansinger. But now Larry has decided to head into something called “non-retirement,” and Sass Linneken is taking over at ROSC. Larry is a longtime WTR and keeps the Maine WTR Resource Center alive. His recent bumpersticker idea: “Divest from the Pentagon” with subtitle “don’t pay federal income taxes.” We are grateful for Larry’s support and assistance to NWTRCC for so many years and look forward to working together in new ways.

Inspiration for A Better World

The U.S. Social Forum (USSF) took place from June 24–28 in three locations: San Jose, Philadelphia, and Jackson, Mississippi. NWTRCC offered workshops and had literature tables in San Jose (Erica Weiland, Cathy Deppe, Anne Barron, and Steve Leeds) and Philadelphia (Ruth Benn, Ari Rosenberg, and Nadine Hoover). Our workshops were small and overall attendance hovered around 1,500 at each site, but we all had good conversations with people aware of and interested in war tax resistance.

Erica found a highlight of the weekend was the People’s Movement Assembly on militarization at home and abroad. Organizers from BAYAN USA and Women for Genuine Security, among other organizations, discussed U.S. militarization in Japan, Korea, and the Philippines. An organizer from Black Alliance for Just Immigration also spoke about militarization at home and some issues in current movements. Erica notes, “I think it’s important that calls for “unity” in the antiwar movement recognize our many organizations’ individual strengths and focuses. This leads to the question, How can we maintain our work in the areas that are most important to each of us while advancing common goals?”

In Philadelphia our time was curtailed by scheduling conflicts, but it was an excellent opportunity to attend a variety of workshops and see who’s doing what, get ideas from how other groups organize, and consider how war tax resistance might be a more visible presence and partner in the movement for peace and social change. Alternative economics was a topic of many workshops and assemblies. In NWTRCC we had begun to do some presentations under the topic of “economic disobedience” and that would have fit in well with many other offerings at the USSF.

Ari said, “Generally I felt like despite the low turn-out people tended to be interested in asking questions and learning more about WTR and that gives me hope that we’ll be able to spread our network as we continue to outreach and build community across social/political spheres.”

Read more about NWTRCC at the USSF on War Tax Talk, nwtrcc.org/blog.

Meet WTRs Somewhere in the U.S.

We look forward to seeing a lot of you at the next NWTRCC Gathering November 6-8, 2015. We try to set locations well in advance, but invitations were scarce this year. Chances lean toward Las Vegas. Our friends at Las Vegas Catholic Worker have us penciled in. At the same time we are waiting to hear from potential hosts in New Orleans. By the time you read this, a decision should have been made. See our website or contact the office, (800) 269-7464, for more details and a brochure.

Profile

War Tax Resistance and Other Paths to a Better World

By Sylvia Metzler

In 2014 my taxable income was $11,826 and I got a $41 refund. Too bad! I would like to have withheld some taxes to protest money used for wars and drone killings and budget cuts for education, health care, and environmental protection. I can no longer concentrate my protests only on military spending. These other issues are just as important and are, of course, related.

In 2014 my taxable income was $11,826 and I got a $41 refund. Too bad! I would like to have withheld some taxes to protest money used for wars and drone killings and budget cuts for education, health care, and environmental protection. I can no longer concentrate my protests only on military spending. These other issues are just as important and are, of course, related.

But can you believe that I once supported the Viet Nam War? That I actually believed in the “domino theory” and was a Rockefeller Republican? The pastor of my Presbyterian Church and his wife changed all that—thank goodness—as they took courageous stands against the war and racism.

As my indignation rose with my education, I took my first timid steps in tax resistance by withholding the federal part of my telephone tax. It felt scary but there were no consequences that I know of.

As the war raged, I heard about people withholding money from their federal tax returns. It gave me a lot of satisfaction to withhold small amounts and to write about my opposition all over the tax form. I also claimed additional allowances on my W-4 so I would owe more taxes at filing time. I kept increasing my tax refusal even though I accumulated interest and penalties, which the IRS sooner or later seized from my savings account or salary. I know some people were able to hide their assets, but I was a single mother with a salaried job and could not figure out a way to do that.

After 1983 when the IRS decided our protests were frivolous (FRIVOLOUS!) I stopped writing on the tax form. I did include a separate letter stating why I was not paying all the taxes that I owed but did not want to risk fines.

As the Viet Nam War was coming to a close, I turned to my Pennsylvania state tax return. The death penalty was reinstituted here in 1973 and was being used, so I started to withhold money from my state tax return. I also protested the death penalty at the District Attorney’s office in Philadelphia and spent a week in county jail in 1998 for blocking the doors with four other activists.

During the first Gulf War in 1991, I was working in Nicaragua as a volunteer nurse practitioner. Many of us protested by fasting to call attention to the criminality of that action. I was way under the taxable income then, but when I returned to the U.S., I began to have a decent income again.

Come the wars in Afghanistan and Iraq, we protested at the Federal Building in Philadelphia by the hundreds. Many of us spent a week in federal prison as we refused to pay the fines. I also began my tax resistance again to protest all the tax dollars used for killing and wars. Again the IRS eventually seized my assets to pay the tax, interest, and penalties. I was able to afford that but have always contributed to the War Tax Resisters Penalty Fund to help out resisters who owe more than they can afford to lose.

I wonder sometimes “does it do any good?” But the option of paying taxes without protest or question does not feel good. And tax resistance is but one strategy that we need to use to work for peace and justice in our country and the world.

Sylvia Metzler lives in Philadelphia and is active with many groups including WILPF, Health Care for All PA, Brandywine Peace Community, Medicines for Nicaragua, and Food and Water Watch.